Billionaire Investor Increases Stake in Nvidia Amid Growing Confidence in AI

Third Point's Investment in NVIDIA: Dan Loeb's Third Point LLC increased its stake in NVIDIA Corporation by 2% in Q3 2025, raising its holdings to 2.85 million shares, following an initial acquisition of 1.45 million shares in Q1 2025.

NVIDIA's Strong Earnings Report: NVIDIA reported a 62% year-over-year revenue increase to $57 billion for Q3, surpassing expectations, and provided a positive revenue outlook for Q4, driven by strong demand for its AI chips.

Strategic Partnerships and Investments: NVIDIA expanded its partnership with HUMAIN in Saudi Arabia for AI infrastructure and invested $2 billion in Synopsys, while also enhancing its collaboration with Amazon Web Services.

Stock Performance Comparison: Year-to-date, NVIDIA shares have risen 28.4%, performing comparably to industry peers and ETFs, with significant growth noted in the semiconductor sector overall.

Trade with 70% Backtested Accuracy

Analyst Views on SNPS

About SNPS

About the author

Compass Pathways Reports Positive Trial Data; Salesforce Unveils $1B Investment Plan

- COMP360 Trial Progress: Compass Pathways reported positive results from its Phase 3 COMP006 trial for treatment-resistant depression, showing rapid onset and durable clinical benefits in a 581-patient study, leading to an approximately 8% premarket stock increase and bolstering late-stage development prospects.

- Salesforce Investment Plan: Salesforce announced a $1 billion investment in Switzerland over the next five years to accelerate the adoption of agentic AI, which will expand its local workforce, customer ecosystem, and AI skills initiatives, as revealed by CEO Marc Benioff at the AI for Good Global Summit, enhancing the company's competitive edge.

- Synopsys Strategic Shift: Synopsys advanced 0.83% in premarket trading after plans to discontinue parts of its manufacturing process control software business and redirect resources toward higher-margin AI design products, having informed over 10 semiconductor manufacturers about halting new version releases while continuing support under existing contracts, indicating a strong focus on AI.

- Autodesk Acquisition Update: Autodesk rose 1.2% in premarket trading following the FTC's early termination of its review of the MaintainX acquisition, which is expected to strengthen its industrial asset management and operations software capabilities, further solidifying its market position.

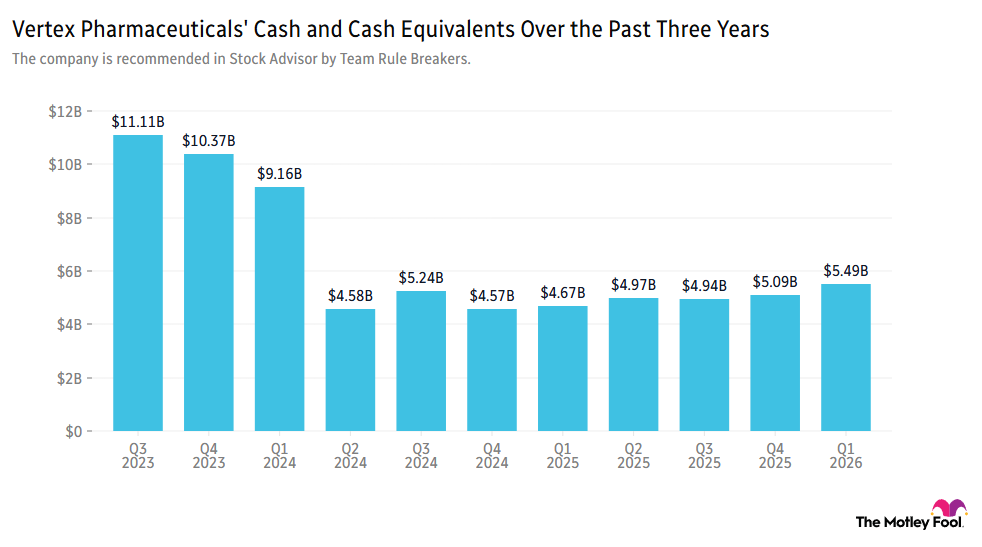

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

Synopsys Discontinues Manufacturing Software to Focus on AI Design

- Software Discontinuation Notice: Synopsys has informed over 10 chipmakers, including Samsung and SK Hynix, about the decision to cease updates and support for a suite of manufacturing process control software, which is expected to impact production efficiency.

- Resource Reallocation: The company is reallocating resources to higher-margin AI design products, although this move may lead to insufficient maintenance and updates for production tools, potentially affecting production yields.

- Layoff Impact: The layoffs associated with the software discontinuation have involved several dozen employees, highlighting the company's focus on cost control during its transition while also reflecting a reduction in its traditional product lines.

- Customer Reactions: While some customers like Samsung have developed alternative tools and stated there will be no negative impact on production, concerns remain regarding the potential production risks associated with the discontinuation of the software.

Synopsys Upgraded to Overweight by Piper Sandler

- Rating Upgrade: Piper Sandler upgraded Synopsys, Inc. (NASDAQ:SNPS) from Neutral to Overweight, raising the price target from $450 to $550, reflecting optimism about the recovery of its intellectual property business.

- Customer Demand Recovery: Analyst Clarke Jeffries noted that Intel's 18A-P manufacturing node is seen as a practical alternative to constrained TSMC capacity, which is expected to accelerate the recovery of intellectual property demand at Synopsys' largest customer, Intel.

- Board Changes: Synopsys reached a settlement with Elliott Investment Management, appointing managing partner Jesse Cohn to its board and expanding the board to 11 members, indicating proactive adjustments in corporate governance.

- AI Investment Outlook: Cohn stated that Synopsys is moving in a direction to benefit from rising AI investments and growing engineering complexity, although analysts believe certain AI stocks offer greater upside potential and less downside risk.

Major Rating Changes on Wall Street

- IBM Upgrade: JPMorgan upgraded IBM from Neutral to Overweight, citing a deeper analysis of its software business that suggests significant performance acceleration in 2H'26, thereby enhancing market confidence in the company's growth trajectory.

- Qiagen Upgrade: Morgan Stanley upgraded Qiagen from Equal Weight to Overweight, noting that AI-driven growth improvements and the clearing of competitive risks are expected to positively impact the life sciences sector.

- Smurfit Westrock Initiation: Deutsche Bank initiated coverage of Smurfit Westrock with a Buy rating and a $57 price target, emphasizing its high-margin operations and strong market position as catalysts for value creation in the packaging industry.

- Target Upgrade: Wolfe upgraded Target from Peer Perform to Outperform, stating that now is the optimal time to buy, as the company is poised for significant improvements driven by store resets and a new leadership team shaking up the status quo.

Synopsys Launches New Multiphysics Fusion Platform for AI Chip Design

- Platform Launch: Synopsys announced the launch of its new Multiphysics Fusion platform on June 17, combining AI-powered chip design tools with Ansys analysis technology to expedite the development of advanced AI chips, enhancing market competitiveness.

- Performance Boost: The platform delivers up to 3x faster timing signoff and 10x faster design closure, with early users like MediaTek reporting runtimes that are 10 times faster than before, indicating significant efficiency gains.

- Customer Validation: The technology has been validated by companies such as NVIDIA, Samsung Electronics, MediaTek, and Cisco, with NVIDIA's pilot designs achieving up to 5x faster design closure and 86% IR fix rates, demonstrating its effectiveness in real-world applications.

- Market Impact: Although Synopsys stock is currently trading slightly lower at around $458.61, the launch of the new platform could serve as a positive catalyst, especially if customer adoption and AI semiconductor spending remain strong.

Compass Pathways Reports Positive Trial Data; Salesforce Unveils $1B Investment Plan

- COMP360 Trial Progress: Compass Pathways reported positive results from its Phase 3 COMP006 trial for treatment-resistant depression, showing rapid onset and durable clinical benefits in a 581-patient study, leading to an approximately 8% premarket stock increase and bolstering late-stage development prospects.

- Salesforce Investment Plan: Salesforce announced a $1 billion investment in Switzerland over the next five years to accelerate the adoption of agentic AI, which will expand its local workforce, customer ecosystem, and AI skills initiatives, as revealed by CEO Marc Benioff at the AI for Good Global Summit, enhancing the company's competitive edge.

- Synopsys Strategic Shift: Synopsys advanced 0.83% in premarket trading after plans to discontinue parts of its manufacturing process control software business and redirect resources toward higher-margin AI design products, having informed over 10 semiconductor manufacturers about halting new version releases while continuing support under existing contracts, indicating a strong focus on AI.

- Autodesk Acquisition Update: Autodesk rose 1.2% in premarket trading following the FTC's early termination of its review of the MaintainX acquisition, which is expected to strengthen its industrial asset management and operations software capabilities, further solidifying its market position.

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

Synopsys Discontinues Manufacturing Software to Focus on AI Design

- Software Discontinuation Notice: Synopsys has informed over 10 chipmakers, including Samsung and SK Hynix, about the decision to cease updates and support for a suite of manufacturing process control software, which is expected to impact production efficiency.

- Resource Reallocation: The company is reallocating resources to higher-margin AI design products, although this move may lead to insufficient maintenance and updates for production tools, potentially affecting production yields.

- Layoff Impact: The layoffs associated with the software discontinuation have involved several dozen employees, highlighting the company's focus on cost control during its transition while also reflecting a reduction in its traditional product lines.

- Customer Reactions: While some customers like Samsung have developed alternative tools and stated there will be no negative impact on production, concerns remain regarding the potential production risks associated with the discontinuation of the software.

Synopsys Upgraded to Overweight by Piper Sandler

- Rating Upgrade: Piper Sandler upgraded Synopsys, Inc. (NASDAQ:SNPS) from Neutral to Overweight, raising the price target from $450 to $550, reflecting optimism about the recovery of its intellectual property business.

- Customer Demand Recovery: Analyst Clarke Jeffries noted that Intel's 18A-P manufacturing node is seen as a practical alternative to constrained TSMC capacity, which is expected to accelerate the recovery of intellectual property demand at Synopsys' largest customer, Intel.

- Board Changes: Synopsys reached a settlement with Elliott Investment Management, appointing managing partner Jesse Cohn to its board and expanding the board to 11 members, indicating proactive adjustments in corporate governance.

- AI Investment Outlook: Cohn stated that Synopsys is moving in a direction to benefit from rising AI investments and growing engineering complexity, although analysts believe certain AI stocks offer greater upside potential and less downside risk.

Major Rating Changes on Wall Street

- IBM Upgrade: JPMorgan upgraded IBM from Neutral to Overweight, citing a deeper analysis of its software business that suggests significant performance acceleration in 2H'26, thereby enhancing market confidence in the company's growth trajectory.

- Qiagen Upgrade: Morgan Stanley upgraded Qiagen from Equal Weight to Overweight, noting that AI-driven growth improvements and the clearing of competitive risks are expected to positively impact the life sciences sector.

- Smurfit Westrock Initiation: Deutsche Bank initiated coverage of Smurfit Westrock with a Buy rating and a $57 price target, emphasizing its high-margin operations and strong market position as catalysts for value creation in the packaging industry.

- Target Upgrade: Wolfe upgraded Target from Peer Perform to Outperform, stating that now is the optimal time to buy, as the company is poised for significant improvements driven by store resets and a new leadership team shaking up the status quo.

Synopsys Launches New Multiphysics Fusion Platform for AI Chip Design

- Platform Launch: Synopsys announced the launch of its new Multiphysics Fusion platform on June 17, combining AI-powered chip design tools with Ansys analysis technology to expedite the development of advanced AI chips, enhancing market competitiveness.

- Performance Boost: The platform delivers up to 3x faster timing signoff and 10x faster design closure, with early users like MediaTek reporting runtimes that are 10 times faster than before, indicating significant efficiency gains.

- Customer Validation: The technology has been validated by companies such as NVIDIA, Samsung Electronics, MediaTek, and Cisco, with NVIDIA's pilot designs achieving up to 5x faster design closure and 86% IR fix rates, demonstrating its effectiveness in real-world applications.

- Market Impact: Although Synopsys stock is currently trading slightly lower at around $458.61, the launch of the new platform could serve as a positive catalyst, especially if customer adoption and AI semiconductor spending remain strong.