UPS Stock Rises Amid Positive Turnaround Outlook

UPS's stock increased by 5.01% as it crossed above the 5-day SMA, reflecting growing investor confidence in its turnaround strategy.

Despite expectations of weak earnings in the first half of 2026, UPS has communicated a positive outlook for the second half, indicating potential recovery. The company has seen a steady increase in revenue per piece in its U.S. business, which is a key indicator of its early turnaround success. This optimism is encouraging investors to consider buying before the upcoming earnings report, as the stock has rebounded 30% from its lows in October 2025.

The implications of this turnaround plan suggest that UPS is on a path to recovery, which could lead to further stock appreciation as market confidence builds ahead of the earnings report.

Trade with 70% Backtested Accuracy

Analyst Views on UPS

About UPS

About the author

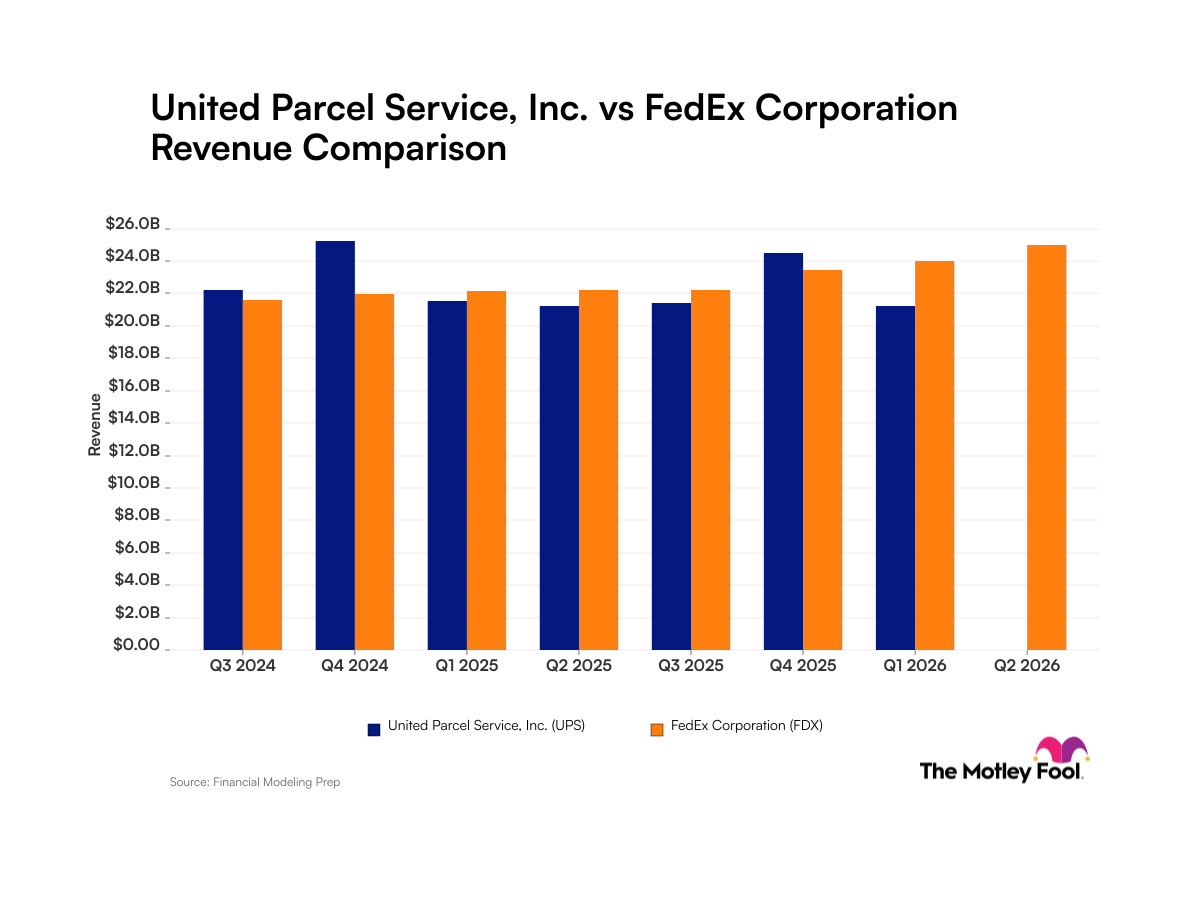

Analysis of Revenue Fluctuations for UPS and FedEx

- UPS Revenue Fluctuations: UPS reported a 4% net income margin for Q1 2026 while planning to close additional distribution centers; despite significant revenue from Amazon, the partnership was cut due to low margins, leading to increased quarterly revenue volatility and impacting overall profitability.

- FedEx Growth Momentum: FedEx achieved $94.7 billion in revenue for the fiscal year ending May 31, 2026, a notable increase from $87.9 billion the previous year, with an expected year-over-year growth of approximately 11% in the next fiscal year, indicating strong competitive positioning and expansion potential.

- Industry Comparison: UPS focuses on margin protection due to higher union costs, limiting revenue growth, while FedEx prioritizes volume growth to expand sales, highlighting significant strategic differences between the two companies.

- Market Dynamics Impact: UPS's revenue fluctuations are closely tied to its strategy of cutting low-margin business, while FedEx's spin-off of its freight division may further drive revenue growth, reflecting differing strategies in responding to market changes.

FedEx vs UPS: Revenue Trends Analysis

- Revenue Growth Comparison: FedEx has consistently achieved revenue growth over the past eight quarters, reporting $94.7 billion for fiscal year 2026, an 8% increase from $87.9 billion the previous year, demonstrating its stable business expansion capabilities.

- UPS Volatile Performance: In contrast, UPS experienced significant quarterly fluctuations during the same period, with a net income margin of 4% for Q1 2026, as it reduced its low-margin partnership with Amazon, leading to unstable revenue and impacting overall profitability.

- Strategic Market Differences: FedEx prioritizes volume growth, expecting approximately 11% year-over-year growth in the next fiscal year, while UPS focuses on margin protection due to higher union costs, limiting its revenue growth potential.

- Investor Considerations: Analysts advise investors to consider the impact of UPS's reduced collaboration with Amazon on its revenue before investing, while FedEx's spin-off of its freight business may further enhance its market share.

Multiple Companies Face Dividend Cut Risks

- Dividend Cut Risks: According to Wolfe Research, several companies are at risk of cutting dividends, particularly those with high debt levels and payout ratios exceeding 80%, which could directly impact income investors' cash flow.

- Whirlpool's Dividend Suspension: Whirlpool announced in May that it would suspend its dividend to pay down debt and navigate what it termed a 'recession-level industry decline,' reflecting the company's strategy under financial pressure, which may affect shareholder confidence.

- PepsiCo's Dividend Increase: Despite increasing its dividend in June, PepsiCo, with a 4.14% yield, appeared on Wolfe's screen, and its second-quarter earnings report is expected this Thursday, with analysts maintaining an optimistic outlook, indicating market confidence in its stability.

- UPS's Turnaround Plan: United Parcel Service (UPS) currently has a 5.95% dividend yield and aims for $3 billion in annual cost savings by 2026; despite challenges, its stock has risen 11% year-to-date, reflecting market recognition of its turnaround efforts.

UPS Invests $48 Million to Upgrade Facilities

- Strategic Investment: UPS plans to invest $48 million in 27 temperature-controlled facilities to meet the growing demand for low-temperature medication transport, particularly GLP-1 weight-loss drugs, highlighting the company's strategic focus on the healthcare sector.

- Business Transformation: Despite a 50% drop in stock price from its 2022 peak, UPS is undergoing a massive business overhaul aimed at enhancing operational efficiency through modernization, although this may lead to short-term revenue declines and increased costs.

- Customer Focus: UPS is shifting from low-margin customers to high-margin ones, particularly in the healthcare sector, which is expected to yield higher profit margins and growth opportunities, reflecting the company's emphasis on future profitability.

- Market Reaction: Although investors remain cautious about UPS's turnaround, resulting in a high 6% dividend yield, the $48 million investment indicates a long-term strategic effort towards growth, potentially leading to a business inflection point in the second half of 2026.

UPS Invests $48 Million in Temperature-Controlled Facilities

- Business Transformation Investment: UPS has announced a $48 million investment in 27 temperature-controlled facilities to meet the rising demand for low-temperature medication transport, particularly GLP-1 weight-loss drugs, thereby enhancing its market share and profit margins in the healthcare sector.

- Customer Focus Strategy: The company is shifting from low-margin high-volume customers to high-margin clients, which has led to a decline in overall revenue; however, revenue per package is increasing, indicating early signs of success, with management projecting a turnaround inflection point in the second half of 2026.

- Market Reaction and Dividends: Despite UPS's stock price dropping 50% from its 2022 peak, its 6% dividend yield reflects investor concerns about the turnaround, while also indicating market expectations for future growth potential.

- Long-term Strategic Significance: By investing in temperature-controlled facilities, UPS is not only enhancing service quality but also laying the groundwork for future growth, particularly in high-margin opportunities within the healthcare sector, signaling a potential shift from business contraction to expansion.

Jim Cramer Increases FedEx Holdings

- Increased Holdings: Jim Cramer's Charitable Trust purchased 130 shares of FedEx shortly after the market opened, raising its total holdings to 230 shares and increasing its portfolio weight from 0.75% to 1.75%, reflecting confidence in FedEx's future performance.

- Earnings Beat: FedEx's latest earnings report exceeded analyst expectations, with both revenue and adjusted earnings per share (EPS) performing well, although management's guidance was complicated by the company's restructuring, impacting investor assessments.

- Future Outlook: FedEx guided for adjusted EPS in the range of $16.90 to $18.10 for calendar year 2026, slightly below some analysts' expectations, yet management anticipates a 20% year-over-year growth during the transition period, showcasing strong business momentum.

- Margin Impact: CEO Raj Subramaniam noted that excluding fuel surcharges would have led to year-over-year margin increases, despite the surcharges negatively affecting profits and making reported results appear softer than their true nature.

Analysis of Revenue Fluctuations for UPS and FedEx

- UPS Revenue Fluctuations: UPS reported a 4% net income margin for Q1 2026 while planning to close additional distribution centers; despite significant revenue from Amazon, the partnership was cut due to low margins, leading to increased quarterly revenue volatility and impacting overall profitability.

- FedEx Growth Momentum: FedEx achieved $94.7 billion in revenue for the fiscal year ending May 31, 2026, a notable increase from $87.9 billion the previous year, with an expected year-over-year growth of approximately 11% in the next fiscal year, indicating strong competitive positioning and expansion potential.

- Industry Comparison: UPS focuses on margin protection due to higher union costs, limiting revenue growth, while FedEx prioritizes volume growth to expand sales, highlighting significant strategic differences between the two companies.

- Market Dynamics Impact: UPS's revenue fluctuations are closely tied to its strategy of cutting low-margin business, while FedEx's spin-off of its freight division may further drive revenue growth, reflecting differing strategies in responding to market changes.

FedEx vs UPS: Revenue Trends Analysis

- Revenue Growth Comparison: FedEx has consistently achieved revenue growth over the past eight quarters, reporting $94.7 billion for fiscal year 2026, an 8% increase from $87.9 billion the previous year, demonstrating its stable business expansion capabilities.

- UPS Volatile Performance: In contrast, UPS experienced significant quarterly fluctuations during the same period, with a net income margin of 4% for Q1 2026, as it reduced its low-margin partnership with Amazon, leading to unstable revenue and impacting overall profitability.

- Strategic Market Differences: FedEx prioritizes volume growth, expecting approximately 11% year-over-year growth in the next fiscal year, while UPS focuses on margin protection due to higher union costs, limiting its revenue growth potential.

- Investor Considerations: Analysts advise investors to consider the impact of UPS's reduced collaboration with Amazon on its revenue before investing, while FedEx's spin-off of its freight business may further enhance its market share.

Multiple Companies Face Dividend Cut Risks

- Dividend Cut Risks: According to Wolfe Research, several companies are at risk of cutting dividends, particularly those with high debt levels and payout ratios exceeding 80%, which could directly impact income investors' cash flow.

- Whirlpool's Dividend Suspension: Whirlpool announced in May that it would suspend its dividend to pay down debt and navigate what it termed a 'recession-level industry decline,' reflecting the company's strategy under financial pressure, which may affect shareholder confidence.

- PepsiCo's Dividend Increase: Despite increasing its dividend in June, PepsiCo, with a 4.14% yield, appeared on Wolfe's screen, and its second-quarter earnings report is expected this Thursday, with analysts maintaining an optimistic outlook, indicating market confidence in its stability.

- UPS's Turnaround Plan: United Parcel Service (UPS) currently has a 5.95% dividend yield and aims for $3 billion in annual cost savings by 2026; despite challenges, its stock has risen 11% year-to-date, reflecting market recognition of its turnaround efforts.

UPS Invests $48 Million to Upgrade Facilities

- Strategic Investment: UPS plans to invest $48 million in 27 temperature-controlled facilities to meet the growing demand for low-temperature medication transport, particularly GLP-1 weight-loss drugs, highlighting the company's strategic focus on the healthcare sector.

- Business Transformation: Despite a 50% drop in stock price from its 2022 peak, UPS is undergoing a massive business overhaul aimed at enhancing operational efficiency through modernization, although this may lead to short-term revenue declines and increased costs.

- Customer Focus: UPS is shifting from low-margin customers to high-margin ones, particularly in the healthcare sector, which is expected to yield higher profit margins and growth opportunities, reflecting the company's emphasis on future profitability.

- Market Reaction: Although investors remain cautious about UPS's turnaround, resulting in a high 6% dividend yield, the $48 million investment indicates a long-term strategic effort towards growth, potentially leading to a business inflection point in the second half of 2026.

UPS Invests $48 Million in Temperature-Controlled Facilities

- Business Transformation Investment: UPS has announced a $48 million investment in 27 temperature-controlled facilities to meet the rising demand for low-temperature medication transport, particularly GLP-1 weight-loss drugs, thereby enhancing its market share and profit margins in the healthcare sector.

- Customer Focus Strategy: The company is shifting from low-margin high-volume customers to high-margin clients, which has led to a decline in overall revenue; however, revenue per package is increasing, indicating early signs of success, with management projecting a turnaround inflection point in the second half of 2026.

- Market Reaction and Dividends: Despite UPS's stock price dropping 50% from its 2022 peak, its 6% dividend yield reflects investor concerns about the turnaround, while also indicating market expectations for future growth potential.

- Long-term Strategic Significance: By investing in temperature-controlled facilities, UPS is not only enhancing service quality but also laying the groundwork for future growth, particularly in high-margin opportunities within the healthcare sector, signaling a potential shift from business contraction to expansion.

Jim Cramer Increases FedEx Holdings

- Increased Holdings: Jim Cramer's Charitable Trust purchased 130 shares of FedEx shortly after the market opened, raising its total holdings to 230 shares and increasing its portfolio weight from 0.75% to 1.75%, reflecting confidence in FedEx's future performance.

- Earnings Beat: FedEx's latest earnings report exceeded analyst expectations, with both revenue and adjusted earnings per share (EPS) performing well, although management's guidance was complicated by the company's restructuring, impacting investor assessments.

- Future Outlook: FedEx guided for adjusted EPS in the range of $16.90 to $18.10 for calendar year 2026, slightly below some analysts' expectations, yet management anticipates a 20% year-over-year growth during the transition period, showcasing strong business momentum.

- Margin Impact: CEO Raj Subramaniam noted that excluding fuel surcharges would have led to year-over-year margin increases, despite the surcharges negatively affecting profits and making reported results appear softer than their true nature.