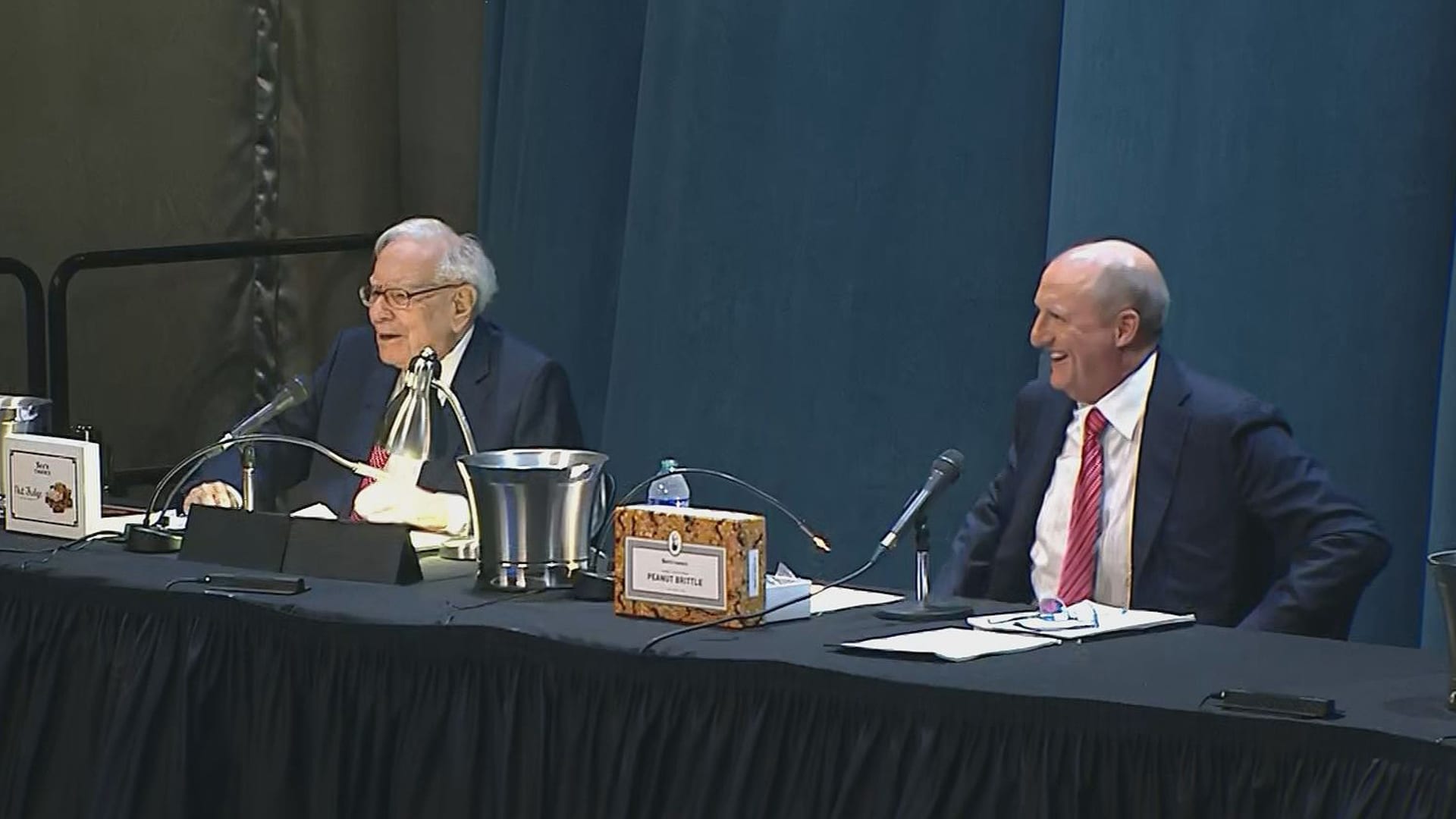

Buffett's Stable Investment Choices

Written by Emily J. Thompson, Senior Investment Analyst

Updated: May 08 2026

0mins

Source: Fool

- Credit Card Payment Growth: U.S. retail spending rose 3.7% last quarter despite rising prices, with Visa reporting a 9% increase in total payment volume, driving a 17% year-over-year revenue growth, indicating a sustained consumer reliance on credit cards and reflecting potential economic recovery.

- VeriSign's Stability: VeriSign achieved $1.66 billion in revenue last year, up 6.4%, with net income of $8.81 per share; while growth is slow, its monopoly in global domain management ensures long-term profitability and resilience against economic fluctuations.

- Coca-Cola's Consistent Returns: Coca-Cola, as Berkshire's third-largest holding valued over $30 billion, boasts a 64-year track record of consecutive dividend increases, demonstrating strong cash flow capabilities that provide stable support for investments during economic uncertainty.

- Buffett's Investment Philosophy: Although Buffett stepped down as CEO last year, his investment choices continue to dominate Berkshire's portfolio, emphasizing the importance of quality investing amidst market volatility and encouraging investors to focus on long-term value.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy VRSN?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on VRSN

Wall Street analysts forecast VRSN stock price to rise

3 Analyst Rating

2 Buy

1 Hold

0 Sell

Moderate Buy

Current: 259.130

Low

271.00

Averages

311.00

High

337.00

Current: 259.130

Low

271.00

Averages

311.00

High

337.00

About VRSN

VeriSign, Inc. is a provider of critical internet infrastructure and domain name registry services, enabling internet navigation for various domain names. The Company helps to enable the security, stability, and resiliency of the domain name system (DNS) and the Internet by providing root zone maintainer services, operating two of the 13 global Internet root servers, and providing registration services and authoritative resolution. It operates the authoritative directory for all .com, .net, and .name domain names (generic top-level domains or gTLDs), as well as for certain transliterations of .com and .net in a number of different native languages and scripts (internationalized). It also operates the authoritative directory for all .cc domain names (country code top-level domain or ccTLD). The Company operates the technical or back-end systems for the .edu top-level domain. Its operations infrastructure includes distributed servers, networking, and disaster recovery plans.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

VeriSign Faces AI Challenges and Contract Renewal Risks

- Monopoly Position: VeriSign operates the core registry infrastructure for .com and .net domains through exclusive regulatory agreements, generating $1.1 billion in free cash flow from $1.7 billion in revenue last year, showcasing its strong pricing power and nearly zero marginal costs.

- AI Impact and Growth: While the adoption of AI has altered how users navigate the internet, management reports that AI tools have lowered the barrier to website creation, driving a 3.7% year-over-year increase in domain registrations in Q1 2026 and tripling DNS traffic over the past three years.

- Contract Renewal Risks: VeriSign's .net and .com contracts are set to expire in 2029 and 2030, respectively; although the company has a presumptive right of renewal, risks around pricing may prompt long-term investors to reassess the stability of its regulatory moat as critical renewals approach.

- Cautious Investor Sentiment: Despite being a high-quality company, the potential impact of AI and uncertainties surrounding contract renewals may lead investors to remain on the sidelines, contributing to the stock's underperformance, which has lagged the broader market by approximately 30% over the past year.

See More

VeriSign Faces AI Transformation and Contract Renewal Risks

- Registration Growth Rebound: AI tools have lowered barriers to website creation, leading to a 3.7% year-over-year growth in VeriSign's domain base in Q1 2026, indicating a recovery in registrations after a stagnation period, thereby enhancing its market competitiveness.

- Strong Cash Flow Performance: Despite modest revenue growth, VeriSign generated $1.7 billion in revenue and $1.1 billion in free cash flow last year, showcasing its robust profitability and capital-light business model as an internet infrastructure provider.

- Contract Renewal Risks: VeriSign's core .com and .net contracts are set to expire in 2029 and 2030, respectively; while the company has a presumptive right of renewal, pricing risks and regulatory uncertainties could impact its future market position.

- AI Impact Uncertainty: The rise of AI chatbots may change how users navigate the internet, and while management argues that these agents will still require stable identifiers to verify content, the long-term value of .com addresses could be threatened.

See More

Digital Brands Group Partners with Outdoor Brand to Combat Counterfeiting

- Strategic Partnership: Digital Brands Group (NASDAQ:DBGI) has formed a strategic alliance with a globally recognized outdoor performance brand to leverage AI technology in addressing the $467 billion global counterfeit issue, thereby solidifying its market position in brand protection.

- Technological Support: This collaboration will utilize SECUR3D's technology to identify unauthorized digital assets and counterfeit products, which is expected to significantly enhance intellectual property protection capabilities across digital marketplaces and bolster consumer trust.

- Market Potential: According to OECD-EUIPO data, 83% of online counterfeiting occurs through social and e-commerce channels, and Digital Brands Group's AI brand protection strategy positions it favorably in the rapidly evolving e-commerce landscape, addressing brands' urgent security needs.

- Strategic Transformation: Digital Brands Group is transitioning from a traditional apparel brand to an AI infrastructure platform, enhancing its capabilities in consumer brand operations and digital asset protection through partnerships with multiple AI companies, which is anticipated to yield long-term growth potential for the company.

See More

Digital Brands Group Partners with Outdoor Brand to Combat Counterfeiting

- Massive Counterfeit Market: According to the latest OECD-EUIPO data, the global counterfeit goods market is estimated at $467 billion, with 83% of online counterfeiting occurring through social and e-commerce channels, highlighting the urgency and importance of brand protection.

- Strategic Partnership Enhancement: Digital Brands Group (NASDAQ:DBGI) has established a new AI and brand protection collaboration with a globally recognized outdoor brand, leveraging SECUR3D's technology to identify unauthorized digital assets and counterfeit-related listings, aiming to enhance brand competitiveness in the market.

- Early Data Reveals Losses: In its first AI brand protection deployment with Herschel Supply Co., SECUR3D's AssetSafe platform identified approximately $500,000 in counterfeit activity during the initial scan phase, underscoring the effectiveness of this technology in safeguarding brand assets.

- Ongoing Technology Strategy Deepening: The CEO of Digital Brands Group stated that AI tools will become increasingly important in rapidly evolving digital commerce environments, and the company will continue to explore technology partnerships related to AI to enhance brand protection and consumer trust.

See More

Berkshire Hathaway Reenters Airline Sector with Delta Stake

- Return to Airlines: Berkshire Hathaway has acquired a stake worth over $2.6 billion in Delta Air Lines, marking its return to the airline industry after exiting entirely during the pandemic in 2020, which reflects confidence in the recovery of the aviation market.

- Portfolio Adjustments: In the first quarter, Berkshire trimmed its stake in Chevron while significantly increasing its investment in Alphabet, now its seventh-largest holding, indicating a strategic shift towards technology stocks.

- Impact of Executive Changes: Following the departure of investment manager Todd Combs, Berkshire sold several stocks last quarter, including a complete exit from Amazon, highlighting the necessity of adjusting investment strategies in response to leadership changes.

- Cash Reserve Challenges: Buffett acknowledged the current investment environment is not ideal, with Berkshire's cash reserves nearing $400 billion; nevertheless, the company resumed stock buybacks in the first quarter, signaling a search for suitable investment opportunities.

See More

Buffett's Stable Investment Choices

- Credit Card Payment Growth: U.S. retail spending rose 3.7% last quarter despite rising prices, with Visa reporting a 9% increase in total payment volume, driving a 17% year-over-year revenue growth, indicating a sustained consumer reliance on credit cards and reflecting potential economic recovery.

- VeriSign's Stability: VeriSign achieved $1.66 billion in revenue last year, up 6.4%, with net income of $8.81 per share; while growth is slow, its monopoly in global domain management ensures long-term profitability and resilience against economic fluctuations.

- Coca-Cola's Consistent Returns: Coca-Cola, as Berkshire's third-largest holding valued over $30 billion, boasts a 64-year track record of consecutive dividend increases, demonstrating strong cash flow capabilities that provide stable support for investments during economic uncertainty.

- Buffett's Investment Philosophy: Although Buffett stepped down as CEO last year, his investment choices continue to dominate Berkshire's portfolio, emphasizing the importance of quality investing amidst market volatility and encouraging investors to focus on long-term value.

See More

VeriSign Faces AI Challenges and Contract Renewal Risks

- Monopoly Position: VeriSign operates the core registry infrastructure for .com and .net domains through exclusive regulatory agreements, generating $1.1 billion in free cash flow from $1.7 billion in revenue last year, showcasing its strong pricing power and nearly zero marginal costs.

- AI Impact and Growth: While the adoption of AI has altered how users navigate the internet, management reports that AI tools have lowered the barrier to website creation, driving a 3.7% year-over-year increase in domain registrations in Q1 2026 and tripling DNS traffic over the past three years.

- Contract Renewal Risks: VeriSign's .net and .com contracts are set to expire in 2029 and 2030, respectively; although the company has a presumptive right of renewal, risks around pricing may prompt long-term investors to reassess the stability of its regulatory moat as critical renewals approach.

- Cautious Investor Sentiment: Despite being a high-quality company, the potential impact of AI and uncertainties surrounding contract renewals may lead investors to remain on the sidelines, contributing to the stock's underperformance, which has lagged the broader market by approximately 30% over the past year.

See More

VeriSign Faces AI Transformation and Contract Renewal Risks

- Registration Growth Rebound: AI tools have lowered barriers to website creation, leading to a 3.7% year-over-year growth in VeriSign's domain base in Q1 2026, indicating a recovery in registrations after a stagnation period, thereby enhancing its market competitiveness.

- Strong Cash Flow Performance: Despite modest revenue growth, VeriSign generated $1.7 billion in revenue and $1.1 billion in free cash flow last year, showcasing its robust profitability and capital-light business model as an internet infrastructure provider.

- Contract Renewal Risks: VeriSign's core .com and .net contracts are set to expire in 2029 and 2030, respectively; while the company has a presumptive right of renewal, pricing risks and regulatory uncertainties could impact its future market position.

- AI Impact Uncertainty: The rise of AI chatbots may change how users navigate the internet, and while management argues that these agents will still require stable identifiers to verify content, the long-term value of .com addresses could be threatened.

See More

Digital Brands Group Partners with Outdoor Brand to Combat Counterfeiting

- Strategic Partnership: Digital Brands Group (NASDAQ:DBGI) has formed a strategic alliance with a globally recognized outdoor performance brand to leverage AI technology in addressing the $467 billion global counterfeit issue, thereby solidifying its market position in brand protection.

- Technological Support: This collaboration will utilize SECUR3D's technology to identify unauthorized digital assets and counterfeit products, which is expected to significantly enhance intellectual property protection capabilities across digital marketplaces and bolster consumer trust.

- Market Potential: According to OECD-EUIPO data, 83% of online counterfeiting occurs through social and e-commerce channels, and Digital Brands Group's AI brand protection strategy positions it favorably in the rapidly evolving e-commerce landscape, addressing brands' urgent security needs.

- Strategic Transformation: Digital Brands Group is transitioning from a traditional apparel brand to an AI infrastructure platform, enhancing its capabilities in consumer brand operations and digital asset protection through partnerships with multiple AI companies, which is anticipated to yield long-term growth potential for the company.

See More

Digital Brands Group Partners with Outdoor Brand to Combat Counterfeiting

- Massive Counterfeit Market: According to the latest OECD-EUIPO data, the global counterfeit goods market is estimated at $467 billion, with 83% of online counterfeiting occurring through social and e-commerce channels, highlighting the urgency and importance of brand protection.

- Strategic Partnership Enhancement: Digital Brands Group (NASDAQ:DBGI) has established a new AI and brand protection collaboration with a globally recognized outdoor brand, leveraging SECUR3D's technology to identify unauthorized digital assets and counterfeit-related listings, aiming to enhance brand competitiveness in the market.

- Early Data Reveals Losses: In its first AI brand protection deployment with Herschel Supply Co., SECUR3D's AssetSafe platform identified approximately $500,000 in counterfeit activity during the initial scan phase, underscoring the effectiveness of this technology in safeguarding brand assets.

- Ongoing Technology Strategy Deepening: The CEO of Digital Brands Group stated that AI tools will become increasingly important in rapidly evolving digital commerce environments, and the company will continue to explore technology partnerships related to AI to enhance brand protection and consumer trust.

See More

Berkshire Hathaway Reenters Airline Sector with Delta Stake

- Return to Airlines: Berkshire Hathaway has acquired a stake worth over $2.6 billion in Delta Air Lines, marking its return to the airline industry after exiting entirely during the pandemic in 2020, which reflects confidence in the recovery of the aviation market.

- Portfolio Adjustments: In the first quarter, Berkshire trimmed its stake in Chevron while significantly increasing its investment in Alphabet, now its seventh-largest holding, indicating a strategic shift towards technology stocks.

- Impact of Executive Changes: Following the departure of investment manager Todd Combs, Berkshire sold several stocks last quarter, including a complete exit from Amazon, highlighting the necessity of adjusting investment strategies in response to leadership changes.

- Cash Reserve Challenges: Buffett acknowledged the current investment environment is not ideal, with Berkshire's cash reserves nearing $400 billion; nevertheless, the company resumed stock buybacks in the first quarter, signaling a search for suitable investment opportunities.

See More

Buffett's Stable Investment Choices

- Credit Card Payment Growth: U.S. retail spending rose 3.7% last quarter despite rising prices, with Visa reporting a 9% increase in total payment volume, driving a 17% year-over-year revenue growth, indicating a sustained consumer reliance on credit cards and reflecting potential economic recovery.

- VeriSign's Stability: VeriSign achieved $1.66 billion in revenue last year, up 6.4%, with net income of $8.81 per share; while growth is slow, its monopoly in global domain management ensures long-term profitability and resilience against economic fluctuations.

- Coca-Cola's Consistent Returns: Coca-Cola, as Berkshire's third-largest holding valued over $30 billion, boasts a 64-year track record of consecutive dividend increases, demonstrating strong cash flow capabilities that provide stable support for investments during economic uncertainty.

- Buffett's Investment Philosophy: Although Buffett stepped down as CEO last year, his investment choices continue to dominate Berkshire's portfolio, emphasizing the importance of quality investing amidst market volatility and encouraging investors to focus on long-term value.

See More